Starting February 11, 2024, New York businesses face new guidelines for applying credit card surcharges. Understanding these changes is crucial for compliance and customer experience. Whether you run a cafe, a boutique, or a service-based business, it’s important to know what’s legal and what’s not when it comes to displaying prices and surcharges.

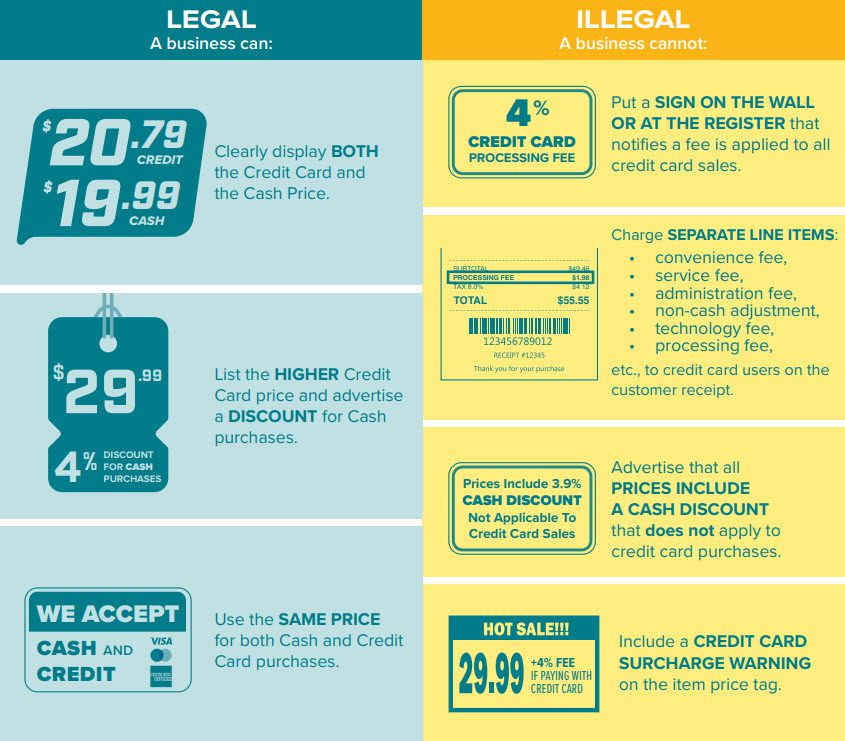

Legal Ways to Apply Surcharges:

- Display Dual Pricing: Clearly show both credit card and cash prices.

- Advertise Cash Discounts: Prominently offer discounts for cash payments over credit card prices.

- Uniform Pricing: Maintain the same price for purchases, irrespective of the payment method.

Practices to Avoid:

- Misleading Signs: Do not post signs that imply a universal fee for all credit card transactions.

- Separate Fees: Avoid itemizing additional fees like service or convenience fees for credit card users.

- Incorrect Advertising: Ensure that all displayed prices are accurate and do not falsely advertise cash discounts for credit card purchases.

This guidance helps protect consumers and keeps businesses clear of legal pitfalls. For detailed examples of correct and incorrect practices, see the included flyer at the top of this post.

Examples of Credit Card Surcharge Practices:

Businesses doing it right:

Sarah’s Stationery

- Practice: Lists dual pricing for items, such as “Notebooks: $10 (Credit) / $9.50 (Cash).”

- Why It Works: Customers appreciate the clarity, making their shopping experience smooth and informed.

Greg’s Groceries

- Practice: Advertises a 3% discount for cash next to credit card prices for every item.

- Why It Works: Encourages cash transactions and maintains price transparency, keeping customers happy and loyal.

The Local Diner

- Practice: Charges the same price for meals, whether paid by cash or credit.

- Why It Works: Simplifies the dining experience, ensuring all customers feel equally treated.

Where businesses need to improve:

Mike’s Movie Theater

- Practice: Displays a sign indicating a “5% fee on all credit card purchases” without detailed pricing.

- Why It’s a Problem: Customers feel misled by the lack of detailed pricing, potentially harming trust and satisfaction.

Fancy Footwear

- Practice: Adds a “Credit Card Handling Fee” of $1.50 visible only at receipt printing.

- Why It’s a Problem: Surprise fees at checkout create a negative last impression, frustrating customers and possibly breaching transparency regulations.

If you have any questions about the credit card surcharge practices or need further clarification on how to implement these guidelines effectively for your business, we’re here to help. Get in touch with us by filling out the form below. We look forward to assisting you in ensuring your business and payment solution comply with regulations and continues to thrive.